United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For

the quarterly period ended

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____ to ____

Commission

File Number

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of Each Class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The

|

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☐ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

The number of outstanding shares of the registrant’s common stock as of August 2, 2021 was .

PROCESSA PHARMACEUTICALS, INC.

TABLE OF CONTENTS

| 2 |

PART 1: FINANCIAL INFORMATION

ITEM 1: FINANCIAL STATEMENTS

Processa Pharmaceuticals, Inc.

Condensed Consolidated Balance Sheets

(Unaudited)

| June 30, 2021 | December 31, 2020 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Due from related party | - | |||||||

| Due from tax agencies | ||||||||

| Prepaid expenses and other | ||||||||

| Total Current Assets | ||||||||

| Property and Equipment, net | - | |||||||

| Other Assets | ||||||||

| Operating lease right-of-use assets, net of accumulated amortization | ||||||||

| Intangible assets, net of accumulated amortization | ||||||||

| Security deposit | ||||||||

| Total Other Assets | ||||||||

| Total Assets | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Note payable – Paycheck Protection Program, current portion | $ | $ | ||||||

| Current maturities of operating lease liability | ||||||||

| Accrued interest | - | |||||||

| Accounts payable | ||||||||

| Due to licensor | ||||||||

| Due to related parties | ||||||||

| Accrued expenses | ||||||||

| Total Current Liabilities | ||||||||

| Non-current Liabilities | ||||||||

| Note payable – Paycheck Protection Program | - | |||||||

| Non-current operating lease liability | ||||||||

| Non-current due to licensor | ||||||||

| Net deferred tax liability | ||||||||

| Total Liabilities | ||||||||

| Commitments and Contingencies | - | - | ||||||

| Stockholders’ Equity | ||||||||

| Common stock, par value $, shares authorized: and issued and outstanding at June 30, 2021 and December 31, 2020, respectively | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Total Stockholders’ Equity | ||||||||

| Total Liabilities and Stockholders’ Equity | $ | $ | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 3 |

Processa Pharmaceuticals, Inc.

Condensed Consolidated Statements of Operations

(Unaudited)

| Three Months Ended | Six Months Ended | |||||||||||||||

| June 30, | June 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Operating Expenses | ||||||||||||||||

| Research and development expenses | $ | $ | $ | $ | ||||||||||||

| Acquisition of in-process research and development | - | - | ||||||||||||||

| General and administrative expenses | ||||||||||||||||

| Operating Loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other Income (Expense) | ||||||||||||||||

| Forgiveness of PPP loan and related accrued interest | - | - | ||||||||||||||

| Interest expense | - | ( | ) | ( | ) | ( | ) | |||||||||

| Interest income | ||||||||||||||||

| Net Operating Loss Before Income Tax Benefit | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Income Tax Benefit | ||||||||||||||||

| Net Loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Net Loss per Common Share - Basic and Diluted | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted Average Common Shares Used to Compute Net Loss Applicable to Common Shares - Basic and Diluted | ||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 4 |

Processa Pharmaceuticals, Inc.

Condensed Consolidated Statement of Changes in Stockholders’ Equity

(Unaudited)

| Six Months Ended June 30, 2021 | ||||||||||||||||||||||||

| Additional | ||||||||||||||||||||||||

| Common Stock | Paid-In | Accumulated | ||||||||||||||||||||||

| Shares | Amount | Capital | Deficit | Total | ||||||||||||||||||||

| Balance at January 1, 2021 | $ | $ | $ | ( | ) | $ | ||||||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||||||

| Shares issued in private placement, net of transaction costs | - | |||||||||||||||||||||||

| Net loss | - | - | - | ( | ) | ( | ) | |||||||||||||||||

| Balance, March 31, 2021 | ( | ) | ||||||||||||||||||||||

| Stock-based compensation | - | |||||||||||||||||||||||

| Shares issued in connection with license agreement | - | |||||||||||||||||||||||

| Net loss | - | - | - | ( | ) | ( | ) | |||||||||||||||||

| Balance, June 30, 2021 | $ | $ | $ | ( | ) | $ | ||||||||||||||||||

| Six Months Ended June 30, 2020 | ||||||||||||||||||||||||

| Additional | Common Stock | |||||||||||||||||||||||

| Common Stock | Paid-In | Dividend | Accumulated | |||||||||||||||||||||

| Shares | Amount | Capital | Payable | Deficit | Total | |||||||||||||||||||

| Balance at January 1, 2020 | $ | $ | $ | $ | ( | ) | $ | |||||||||||||||||

| Stock-based compensation | - | - | - | |||||||||||||||||||||

| Transaction costs related to anticipated 2020 offering | - | - | ( | ) | - | - | ( | ) | ||||||||||||||||

| Net loss | - | - | - | - | ( | ) | ( | ) | ||||||||||||||||

| Balance, March 31, 2020 | ( | ) | ||||||||||||||||||||||

| Stock-based compensation | - | - | - | |||||||||||||||||||||

| Stock dividend distributed due to full-ratchet anti-dilution adjustment | - | ( | ) | - | - | |||||||||||||||||||

| Transaction costs related to anticipated 2020 offering | - | - | ( | ) | - | - | ( | ) | ||||||||||||||||

| Net loss | - | - | - | - | ( | ) | ( | ) | ||||||||||||||||

| Balance, June 30, 2020 | $ | $ | $ | $ | ( | ) | $ | |||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 5 |

Processa Pharmaceuticals, Inc.

Condensed Consolidated Statements of Cash Flows

Six Months Ended June 30, 2021 and 2020

(Unaudited)

| 2021 | 2020 | |||||||

| Cash Flows From Operating Activities | ||||||||

| Net loss | $ | ( |

) | $ | ( |

) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation | ||||||||

| Non-cash lease expense for right-of-use assets | ||||||||

| Non-cash acquisition of in-process research and development | - | |||||||

| Amortization of debt issuance costs | - | |||||||

| Amortization of intangible asset | ||||||||

| Deferred income tax benefit | ( |

) | ( |

) | ||||

| Stock-based compensation | ||||||||

| Forgiveness of PPP loan and related accrued interest | ( | ) | - | |||||

| Net changes in operating assets and liabilities: | ||||||||

| Prepaid expenses and other | ( |

) | ||||||

| Operating lease liability | ( |

) | ( |

) | ||||

| Accrued interest | ||||||||

| Accounts payable | ( |

) | ( |

) | ||||

| Due (from) to related parties | ( |

) | ||||||

| Other receivables | - | |||||||

| Accrued expenses | ||||||||

| Net cash used in operating activities | ( |

) | ( |

) | ||||

| Cash Flows From Financing Activities | ||||||||

| Net proceeds from private placement | - | |||||||

| Borrowings on line of credit payable from related party | - | |||||||

| Proceeds received from our Paycheck Protection Program note payable | - | |||||||

| Other | ( |

) | ( |

) | ||||

| Net cash provided by financing activities | ||||||||

| Net Increase (Decrease) in Cash | ( |

) | ||||||

| Cash and Cash Equivalents – Beginning of Period | ||||||||

| Cash and Cash Equivalents – End of Period | $ | $ | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 6 |

Processa Pharmaceuticals, Inc.

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1 – Organization and Summary of Significant Accounting Policies

Business Activities and Organization

We are a clinical-stage biopharmaceutical company focused on the development of drug products that are intended to provide treatment for patients who have a high unmet medical need condition that effects survival or the patient’s quality of life and for which few or no treatment options currently exist. We currently have five drugs: four in various stages of clinical development (PCS499, PCS12852, PCS3117, and PCS6422) and one in nonclinical development (PCS11T). We group our drugs into non-oncology (PCS499 and PCS12852) and oncology (PCS3117, PCS6422 and PCS11T). A summary of each of our five drugs is provided below:

| ● | Our most advanced product candidate, PCS499, is an oral tablet that is a deuterated analog of one of the major metabolites of pentoxifylline (PTX or Trental®). We completed a Phase 2A trial for PCS499 in patients with ulcerative and non-ulcerative necrobiosis lipoidica (NL) in late 2020, and in May 2021 we enrolled the first patient in our Phase 2B trial for the treatment of ulcerative NL. We expect to complete our interim analysis of the Phase 2B trial in the first half of 2022; complete the trial in the second half of 2022; and, depending on the results, begin a pivotal Phase 3 trial in 2023. | |

| ● | PCS12852 is a highly specific and potent 5HT4 agonist which has already been evaluated in clinical studies in South Korea for gastric emptying and gastrointestinal motility. We are planning on submitting an IND application in the third quarter of 2021 for the treatment of gastroparesis based on our pre-IND communications with the FDA. We anticipate beginning to enroll patients for a Phase 2A trial in the first half of 2022, with expected completion in the first half of 2023. | |

| ● | PCS3117, which we licensed in June 2021, is a cytosine analog, similar to gemcitabine (Gemzar®) but different enough in chemical structure that some patients are more likely to respond to PCS3117 than gemcitabine. We are developing potential biomarkers to predict which patients are more likely to respond to PCS3117 than gemcitabine and other chemotherapy agents to provide a more targeted, precision medicine approach to the treatment of pancreatic and/or non-small cell lung cancer. Over the next 6-12 months, we will be developing and refining these biomarker assays for use in our clinical trials, which should be completed in the first half of 2022. We anticipate validating our approach and confirming our hypothesis in a planned Phase 2B study expected to start in the second half of 2022 and, depending on the results, conducting a Phase 3 pivotal trial in 2023-2024. | |

| ● | PCS6422 is an orally administered irreversible enzyme inhibitor administered in combination with capecitabine. On August 2 2021, we enrolled the first patient in our Phase 1B dose-escalation maximum tolerated dose trial in patients with advanced refractory gastrointestinal (GI) tract tumors. We anticipate completing an interim cohort analysis in the fourth quarter of 2021; determine the maximum tolerated dose (MTD) in the second half of 2022; and, depending on the results, begin a pivotal Phase 2B/3 trial in 2023-2024. | |

| ● | Our only non-clinical asset is PCS11T, an analog of SN38 (SN38 being the active metabolite of irinotecan) and a next generation irinotecan drug for multiple types of cancers. PCS11T is presently in the IND pre-clinical toxicology stage. We hope to submit an IND in the second half of 2022 or first half of 2023, followed by a Phase 1B maximum tolerated dose trial. |

Impact of COVID-19

The extent of the impact of the COVID-19 pandemic on our business, operations and development timelines and plans remains uncertain, and will depend on certain developments, including the duration of the outbreak and its impact on our development activities, planned clinical trial enrollment, future trial sites, contract research organizations (CROs), third-party manufacturers, and other third parties with whom we do business, as well as its impact on regulatory authorities and our key scientific and management personnel. Although we modified our operations and practices in 2020 due to the COVID-19 pandemic and to comply with federal, state and local requirements, our business, operations and development timelines were not materially adversely affected. However, the extent to which the COVID-19 pandemic may affect our business, operations and development timelines and plans in the future, including the resulting impact on our expenditures and capital needs, remains uncertain. In addition, a recession or market correction resulting from the spread of the coronavirus could materially affect the value of our common stock.

| 7 |

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) for interim financial information and with the instructions of the U.S. Securities and Exchange Commission (“SEC”) on Form 10-Q and Article 8 of Regulation S-X.

Accordingly, they do not include all the information and disclosures required by U.S. GAAP for complete financial statements. All material intercompany accounts and transactions have been eliminated in consolidation. In the opinion of management, the accompanying unaudited condensed consolidated financial statements include all adjustments necessary, which are of a normal and recurring nature, for the fair presentation of the Company’s financial position and of the results of operations and cash flows for the periods presented. These condensed consolidated financial statements should be read in conjunction with the audited financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2020, as filed with the SEC. The results of operations for the interim periods shown in this report are not necessarily indicative of the results that may be expected for any other interim period or for the full year.

Liquidity

We

have incurred losses since inception, devoting substantially all of our efforts toward research and development, and have an accumulated

deficit of approximately $

We

had

Use of Estimates

In preparing our condensed consolidated financial statements and related disclosures in conformity with U.S. GAAP and pursuant to the rules and regulations of the SEC, we make estimates and judgments that affect the amounts reported in the condensed consolidated financial statements and accompanying notes. Estimates are used for, but not limited to preclinical and clinical trial expenses, stock-based compensation, intangible assets, future milestone payments and income taxes. These estimates and assumptions are continuously evaluated and are based on management’s experience and knowledge of the relevant facts and circumstances. While we believe the estimates to be reasonable, actual results could differ materially from those estimates and could impact future results of operations and cash flows.

Intangible Assets

Intangible assets acquired individually or with a group of other assets from others (other than in a business combination) are recognized at cost, including transaction costs, and allocated to the individual assets acquired based on relative fair values and no goodwill is recognized. Cost is measured based on cash consideration paid. If consideration given is in the form of non-cash assets, liabilities incurred, or equity interests issued, measurement of cost is based on either the fair value of the consideration given or the fair value of the assets (or net assets) acquired, whichever is more clearly evident and more reliably measurable. Costs of internally developing, maintaining or restoring intangible assets that are not specifically identifiable, have indeterminate lives or are inherent in a continuing business are expensed as incurred.

| 8 |

Intangible assets purchased from others for use in research and development activities and that have alternative future uses (in research and development projects or otherwise) are capitalized in accordance with ASC Topic 350, Intangibles – Goodwill and Other. Those that have no alternative future uses (in research and development projects or otherwise) and therefore no separate economic value are considered research and development costs and are expensed as incurred. Amortization of intangibles used in research and development activities is a research and development cost.

Intangibles with a finite useful life are amortized using the straight-line method unless the pattern in which the economic benefits of the intangible assets are consumed or used up are reliably determinable. The useful life is the best estimate of the period over which the asset is expected to contribute directly or indirectly to our future cash flows. The useful life is based on the duration of the expected use of the asset by us and the legal, regulatory or contractual provisions that constrain the useful life and future cash flows of the asset, including regulatory acceptance and approval, obsolescence, demand, competition and other economic factors. We evaluate the remaining useful life of intangible assets each reporting period to determine whether any revision to the remaining useful life is required. If the remaining useful life is changed, the remaining carrying amount of the intangible asset will be amortized prospectively over the revised remaining useful life. If an income approach is used to measure the fair value of an intangible asset, we consider the period of expected cash flows used to measure the fair value of the intangible asset, adjusted as appropriate for company-specific factors discussed above, to determine the useful life for amortization purposes.

If no regulatory, contractual, competitive, economic or other factors limit the useful life of the intangible to us, the useful life is considered indefinite. Intangibles with an indefinite useful life are not amortized until its useful life is determined to be no longer indefinite. If the useful life is determined to be finite, the intangible is tested for impairment and the carrying amount is amortized over the remaining useful life in accordance with intangibles subject to amortization. Indefinite-lived intangibles are tested for impairment annually and more frequently if events or circumstances indicate that it is more-likely-than-not that the asset is impaired.

Impairment of Long-Lived Assets and Intangibles Other Than Goodwill

We

account for the impairment of long-lived assets in accordance with ASC 360, Property, Plant and Equipment and ASC 350, Intangibles

– Goodwill and Other, which require that long-lived assets and certain identifiable intangibles be reviewed for impairment

whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets

to be held and used is measured by a comparison of the carrying amount of an asset to its expected future undiscounted net cash flows

generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured as the amount by which

the carrying amounts of the assets exceed the fair value of the assets based on the present value of the expected future cash flows associated

with the use of the asset. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell.

Based on management’s evaluation, there was

Stock-based compensation expense is based on the grant-date fair value estimated in accordance with the provisions of ASC 718, Compensation-Stock Compensation. We expense stock-based compensation over the requisite service period based on the estimated grant-date fair value of the awards. Stock-based awards with graded-vesting schedules are recognized on a straight-line basis over the requisite service period for each separately vesting portion of the award. We value restricted stock awards (RSAs) and restricted stock units (RSUs) based on the closing share price on the date of grant. We estimate the fair value of stock option and warrant grants using the Black-Scholes option pricing model, and the assumptions used in calculating the fair value of stock-based awards represent management’s best estimates and involve inherent uncertainties and the application of management’s judgment. Stock-based compensation costs are recorded as general and administrative or research and development costs in the statements of operations based upon the underlying individual’s or consultant’s role.

| 9 |

| Employee and Director stock-based compensation | $ | |||

| Stock-based compensation paid to consultants for services rendered and to be rendered | ||||

| Total amount included in prepaid expenses | ( | ) | ||

| Less amortization of prepaid expenses | ||||

| Total stock-based compensation for the six months ended June 30, 2021 | $ |

At June 30, 2021, $ of stock-based compensation paid to consultants for services is included in our prepaid expense and is being amortized over the contract period of one year as services are expected to be provided.

Basic loss per share is computed by dividing our net loss available to common shareholders by the weighted average number of shares of common stock outstanding and vested RSUs during the period. Diluted loss per share is computed by dividing our net loss available to common shareholders by the diluted weighted average number of shares of common stock during the period. Since we experienced a net loss for both periods presented, basic and diluted net loss per share are the same. As such, diluted loss per share for the six months ended June 30, 2021 and 2020 excludes the impact of potentially dilutive common shares related to outstanding stock options, unvested restricted stock awards (RSAs), unvested restricted stock units (RSUs) and warrants and, in 2020, the conversion of our 2019 Senior Notes and related party line of credit (LOC) since those shares would have an anti-dilutive effect on loss per share.

Our diluted net loss per share for the six months ended June 30, 2021 and 2020 excluded and , respectively, of potentially dilutive common shares, respectively, related to outstanding stock options, unvested RSAs, unvested RSUs and warrants and, in 2020, the conversion of our Senior Notes and related party LOC since those shares would have had an anti-dilutive effect on loss per share during the periods then ended.

Recent Accounting Pronouncements

From time to time, the Financial Accounting Standards Board (“FASB”) or other standard setting bodies issue new accounting pronouncements. Updates to the FASB Accounting Standards Codification are communicated through issuance of an Accounting Standards Update (“ASU”). We have implemented all new accounting pronouncements that are in effect and that may impact our condensed consolidated financial statements. We have evaluated recently issued accounting pronouncements and determined that there is no material impact on our financial position or results of operations.

Note 2 – License Agreement with Ocuphire Pharma, Inc.

On June 16, 2021, we executed a License Agreement with Ocuphire Pharma, Inc. (“Ocuphire Agreement”) under which provided us with a license to research, develop and commercialize PCS3117 (formerly RX-3117) globally, excluding the Republic of Singapore, China, Hong Kong, Macau and Taiwan.

As

consideration for the Ocuphire Agreement, we issued shares of our common stock to Ocuphire,

a cash payment of $

We are required to use commercially reasonable

efforts, at our sole cost and expense to oversee such commercialization efforts, to research, develop and commercialize products

in one or more countries, including meeting

| 10 |

Note 3 – Property and Equipment

Property and equipment at June 30, 2021 and December 31, 2020 consisted of the following:

| June 30, 2021 | December 31, 2020 | |||||||

| Software | $ | $ | ||||||

| Office equipment | ||||||||

| Total Cost | ||||||||

| Less: accumulated depreciation | ||||||||

| Property and equipment, net | $ | $ | ||||||

Note 4 – Intangible Assets

Intangible assets at June 30, 2021 and December 31, 2020 consisted of the following:

June 30, 2021 | December 31, 2020 | |||||||

| Gross intangible assets | $ | $ | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total intangible assets, net | $ | $ | ||||||

Amortization

expense was $

The

capitalized costs for the license rights to PCS499 included the $

Note 5 – Income Taxes

We account for income taxes in accordance with ASC Topic 740, Income Taxes. Deferred income taxes are recorded for the expected tax consequences of temporary differences between the tax basis of assets and liabilities for financial reporting purposes and amounts recognized for income tax purposes. As of June 30, 2021 and December 31, 2020, we recorded a valuation allowance equal to the full recorded amount of our net deferred tax assets related to deferred start-up costs, purchased in-process research and development expenditures, federal orphan drug tax credit and certain other minor temporary differences since it is more-likely-than-not that such benefits will not be realized. The valuation allowance is reviewed quarterly and is maintained until sufficient positive evidence exists to support its reversal.

A

deferred tax liability was recorded on March 19, 2018 when Processa received CoNCERT’s license and “Know-How” in exchange

for Processa stock that had been issued in the Internal Revenue Code Section 351 Transaction. The Section 351 Transaction treats the

acquisition of the license and Know-How for stock as a tax-free exchange. As a result, under ASC 740-10-25-51 Income Taxes, Processa

recorded a deferred tax liability of $

Under ACS 740-270 Income Taxes – Interim Reporting, we are required to project our annual federal and state effective income tax rate and apply it to the year-to-date ordinary operating tax basis loss before income taxes. Based on the projection, we expect to recognize the tax benefit from our projected ordinary tax loss, which can be used to offset the deferred tax liabilities related to the intangible assets and resulted in the recognition of a deferred tax benefit shown in the condensed consolidated statements of operations for three and six months ended June 30, 2021 and 2020. No current income tax expense is expected for the foreseeable future as we expect to generate taxable net operating losses.

| 11 |

We recorded $ and $ of stock-based compensation expense for the six months ended June 30, 2021 and 2020, respectively. During the six months ended June 30, 2021, we awarded the following equity instruments:

| Award Type | Number of Shares Awarded | Number of Shares Vested | ||||||

Restricted stock awards – employee | ||||||||

| Restricted stock units – employees | ||||||||

| Restricted stock units – consultants | ||||||||

| Stock options – consultant | ||||||||

| Warrants – consultant | ||||||||

We valued the RSAs and RSUs based on the closing share price on the date of grant. The fair values of the stock options and warrants granted were estimated using the Black-Scholes option pricing model at the date of grant. The RSUs, stock options and warrants issued to consultants were for services provided in 2021. Of the awards granted to consultants, RSUs and warrants vested upon grant but represent services that will be provided over a one-year service period. As such, at June 30, 2021, we recognized $related to these awards as a prepaid expense for the portion of services the consultant has yet to provide. We did not grant any awards during the same period in 2020.

| Award Type | Amount Outstanding | Amount Vested | Amount Unvested | |||||||||

| Restricted stock awards | ||||||||||||

| Restricted stock units | ||||||||||||

| Stock Options | ||||||||||||

| Warrants | ||||||||||||

The

weighted average exercise price of stock options and warrants outstanding at June 30, 2021 was $ and $, respectively. At June30, 2021, we had warrants for the purchase of

Note 7 – Paycheck Protection Program Loan

In

May 2020, we entered into a $

| 12 |

Note 8 – Stockholders’ Equity

During the six

months ended June 30, 2021 we granted a total of

shares of our common stock and issued a warrant for the purchase of

On

February 24, 2021, we sold in a private placement shares of our common stock to accredited and institutional investors for

gross proceeds of $

On June 16, 2021, we issued shares of our common stock to Ocuphire Pharma, Inc. pursuant to the agreement we entered into with them (see Note 2).

There were issued or outstanding shares of preferred stock at June 30, 2021 or December 31, 2020.

Basic net loss per share is computed by dividing net loss by the weighted average common shares outstanding and vested RSUs. Diluted net loss per share is computed by dividing net loss by the weighted average common shares outstanding, which includes potentially dilutive effect of stock options, unvested RSAs, unvested RSUs, warrants and senior convertible notes. Since we experienced a loss for all periods presented, any dilutive common shares outstanding were excluded from the computation as shown below, as they would have an anti-dilutive impact on diluted net loss per share. The treasury-stock method is used to determine the dilutive effect of our stock options and warrants, and the if-converted method is used to determine the dilutive effect of the Senior Notes.

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Basic and diluted net loss per share: | ||||||||||||||||

| Net loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted average number of common shares-basic and diluted | ||||||||||||||||

| Basic and diluted net loss per share | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

The following potentially dilutive securities were excluded from the computation of diluted net loss per share as their effect would have been anti-dilutive for the periods presented.

| Six months ended June 30, | ||||||||

| 2021 | 2020 | |||||||

| Stock options, unvested RSAs, unvested RSUs and purchase warrants | ||||||||

| Senior convertible notes and convertible related party LOC, plus related accrued interest | ||||||||

Note 10 – Operating Leases

We

lease our office space under an operating lease agreement. This lease does not have significant rent escalation, concessions, leasehold

improvement incentives, or other build-out clauses. Further, the lease does not contain contingent rent provisions. We also lease office

equipment under an operating lease. Our office space lease includes both lease (e.g., fixed payments including rent, taxes, and insurance

costs) and non-lease components (e.g., common-area or other maintenance costs), which are accounted for as a single lease component as

we have elected the practical expedient to group lease and non-lease components for all leases. Our leases do not provide an implicit

rate and, as such, we have used our incremental borrowing rate of

| 13 |

Lease

costs included in our condensed consolidated statements of operations totaled $

| Weighted average remaining lease term (years) for our facility and equipment leases | ||||

| Weighted average discount rate for our facility and equipment leases | % |

Maturities of our lease liabilities for all operating leases were as follows as of June 30, 2021:

| 2021 | $ | |||

| 2022 | ||||

| 2023 | ||||

| 2024 | ||||

| Total lease payments | ||||

| Less: Interest | ( | ) | ||

| Present value of lease liabilities | ||||

| Less: current maturities | ( | ) | ||

| Non-current lease liability | $ |

Note 11 – Related Party Transactions

A

shareholder, CorLyst, LLC, reimburses us for shared costs related to payroll, health care insurance and rent based on actual costs

incurred, which are recognized as a reduction of our general and administrative operating expenses in our condensed consolidated

statement of operations. In September 2020, CorLyst prepaid shared expenses to us for the fourth quarter of 2020 through the July

2021. At June 30, 2021, we recognized $

Note 12 – Commitments and Contingencies

Purchase Obligations

We

enter into contracts in the normal course of business with contract research organizations and subcontractors to further develop our

products and complete our clinical trials. The contracts are cancellable, with varying provisions regarding termination. If we terminated

a cancellable contract with a specific vendor, we would only be obligated for products or services that we received as of the effective

date of the termination and any applicable cancellation fees. We are contractually obligated to pay up to approximately $

| 14 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operation

Forward Looking Statements

This Quarterly Report on Form 10-Q contains “forward-looking statements” that reflect, when made, the Company’s expectations or beliefs concerning future events that involve risks and uncertainties. Forward-looking statements frequently are identified by the words “believe,” “anticipate,” “expect,” “estimate,” “intend,” “project,” “will be,” “will continue,” “will likely result,” or other similar words and phrases. Similarly, statements herein that describe the Company’s objectives, plans or goals also are forward-looking statements. Actual results could differ materially from those projected, implied or anticipated by the Company’s forward-looking statements. Some of the factors that could cause actual results to differ include: our limited operating history, limited cash and history of losses; our ability to achieve profitability; our ability to obtain adequate financing to fund our business operations in the future; the impact of the global pandemic caused by COVID-19, including its impact on our ability to obtain financing or complete clinical trials; our ability to secure required FDA or other governmental approvals for our product candidates and the breadth of the indication sought; the impact of competitive or alternative products, technologies and pricing; whether we are successful in developing and commercializing our technology, including through licensing; the adequacy of protections afforded to us and/or our licensor by the anticipated patents that we own or license and the cost to us of maintaining, enforcing and defending those patents; our and our licensor’s ability to protect non-patented intellectual property rights; our exposure to and ability to defend third-party claims and challenges to our and our licensor’s anticipated patents and other intellectual property rights; and our ability to continue as a going concern. For a discussion of these and all other known risks and uncertainties that could cause actual results to differ from those contained in the forward-looking statements, see “Risk Factors” in the Company’s Annual Report on Form 10-K for the year ended December 31, 2020, which is available on the SEC’s website at www.sec.gov. All forward-looking statements are qualified in their entirety by this cautionary statement, and the Company undertakes no obligation to revise or update this Quarterly Report on Form 10-Q to reflect events or circumstances after the date hereof.

For purposes of this Management’s Discussion and Analysis of Financial Condition and Results of Operations, references to the “Company,” “we,” “us” or “our” refer to the operations of Processa Pharmaceuticals, Inc. and its direct and indirect subsidiaries for the periods described herein.

Overview

We are a clinical-stage biopharmaceutical company focused on the development of drug products that are intended to provide treatment for patients who have a high unmet medical need condition that effects survival or the patient’s quality of life and for which few or no treatment options currently exist.

We are a development company, not a discovery company, that seeks to identify and develop drugs for patients who need better treatment options than presently exist for their medical condition. In order to increase the probability of development success, our pipeline only includes drugs which have previously demonstrated some efficacy in the targeted population or a drug with very similar pharmacological properties has been shown to be effective in the population.

Our screening criteria for identifying and selecting new candidates include:

| ● | addressing an unmet or underserved clinical need, | |

| ● | having demonstrated evidence of efficacy in humans, and | |

| ● | leveraging our regulatory science approach to improve the probability for approval. |

In many instances, these clinical candidates have significant pre-clinical and clinical data that we may leverage to high value inflection points while de-risking the programs and adding in optionality to potential future indications. Our regulatory science approach developed by our team over decades of work with regulatory authorities attempts to balance the “risk/benefit” equation to identify a regulatory path with lower risk and shorter timelines to deliver urgent or unmet medical needs to patients, physicians and caregivers.

Our pipeline includes drugs that (i) already have clinical proof-of-concept data demonstrating the desired pharmacological activity in humans or, minimally, clinical evidence in the form of case studies or clinical experience demonstrating the drug or a similar drug pharmacologically can successfully treat patients with the targeted indication; (ii) target indications for which the FDA believes might allow a single positive pivotal study demonstrating efficacy provides enough evidence that the clinical benefits of the drug and its approval outweighs the risks associated with the drug or the present standard of care (e.g., some orphan indications, many serious life-threatening conditions, some serious quality of life conditions); and/or (iii) target indications where the prevalence of the condition and the likelihood of patients enrolling in a study meet the desired time-frame to demonstrate that the drug can, at some level, treat or potentially treat patients with the condition.

| 15 |

To advance our mission, we have assembled an experienced and successful development team with a track record of drug approvals and successful exits. Our team is experienced in developing drug products through all principal regulatory tiers from IND enabling studies to NDA submission. The combined scientific, development and regulatory experience of our team members has resulted in more than 30 drug approvals by the FDA, over 100 meetings with the FDA and involvement with more than 50 drug development programs, including drug products targeted to patients who have an unmet medical need. Although we believe that the skills and experience of our team members in drug development and commercialization is an important indicator of our future success, the past successes of our team members in developing and commercializing pharmaceutical products does not guarantee that they will successfully develop and commercialize drugs in our current pipeline. In addition, the growth in revenues of companies at which our executive officers and directors served in was due to many factors and does not guarantee that they will successfully operate or manage us or that we will experience similar growth in revenues, even if they continue to serve as executive officers and/or directors.

Our ability to generate meaningful revenue from any products depends on our ability to out-license the drugs before or after we obtain FDA NDA approval. Even if our products are authorized and approved by the FDA, it should be noted that the products must still meet the challenges of successful marketing, distribution and consumer acceptance.

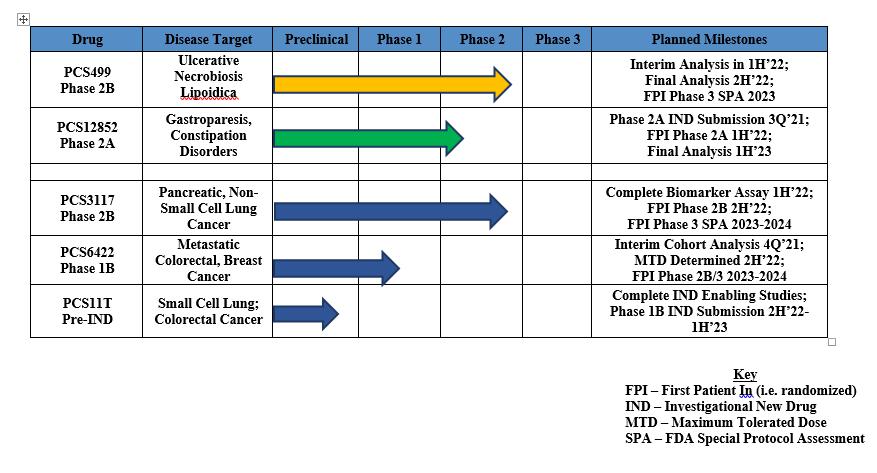

Our Drug Pipeline

Our clinical pipeline (shown below) summarizes each drug, organized by the therapeutic area (i.e., non-oncology and oncology) and stage of development (i.e., Preclinical to Phase 3).

We currently have five drugs: four in various stages of clinical development (PCS499, PCS12852, PCS3117, and PCS6422) and one in nonclinical development (PCS11T). We group our drugs into non-oncology (PCS499 and PCS12852) and oncology (PCS3117, PCS6422 and PCS11T). A summary of each of our five drugs is provided below:

| ● | Our most advanced product candidate, PCS499, is an oral tablet that is a deuterated analog of one of the major metabolites of pentoxifylline (PTX or Trental®). We completed a Phase 2A trial for PCS499 in patients with ulcerative and non-ulcerative necrobiosis lipoidica (NL) in late 2020, and in May 2021 we enrolled the first patient in our Phase 2B trial for the treatment of ulcerative NL. We expect to complete our interim analysis of the Phase 2B trial in the first half of 2022 (1H’22); complete the trial in the second half of 2022 (2H’22); and, depending on the results, begin a pivotal Phase 3 trial in 2023. | |

| ● | PCS12852 is a highly specific and potent 5HT4 agonist which has already been evaluated in clinical studies in South Korea for gastric emptying and gastrointestinal motility. We are planning on submitting an IND application in the third quarter of 2021 (3Q’21) for the treatment of gastroparesis based on our pre-IND communications with the FDA. We anticipate beginning to enroll patients for a Phase 2A trial in the 1H’22, with expected completion in the first half of 2023 (1H’23). | |

| ● | PCS3117, which we licensed in June 2021, is a cytosine analog, similar to gemcitabine (Gemzar®) but different enough in chemical structure that some patients are more likely to respond to PCS3117 than gemcitabine. We are developing potential biomarkers to predict which patients are more likely to respond to PCS3117 than gemcitabine and other chemotherapy agents to provide a more targeted, precision medicine approach to the treatment of pancreatic and/or non-small cell lung cancer. Over the next 6-12 months, we will be developing and refining these biomarker assays for use in our clinical trials, which should be completed in the 1H’22. We anticipate validating our approach and confirming our hypothesis in a planned Phase 2B study expected to start in the 2H’22 and, depending on the results, conducting a Phase 3 pivotal trial in 2023-2024. | |

| ● | PCS6422 is an orally administered irreversible enzyme inhibitor administered in combination with capecitabine. On August 2, 2021, we enrolled the first patient in our Phase 1B dose-escalation maximum tolerated dose trial in patients with advanced refractory gastrointestinal (GI) tract tumors. We anticipate completing an interim cohort analysis in the fourth quarter of 2021 (4Q’21); determine the maximum tolerated dose (MTD) in the second half of 2022; and, depending on the results, begin a pivotal Phase 2B/3 trial in 2023-2024. | |

| · | ● | Our only non-clinical asset is PCS11T, an analog of SN38 (SN38 being the active metabolite of irinotecan) and a next generation irinotecan drug for multiple types of cancers. PCS11T is presently in the IND pre-clinical toxicology stage. We hope to submit an IND in the 2H’22 or 1H’23, followed by a Phase 1B maximum tolerated dose trial. |

| 16 |

PCS499

PCS499, an oral tablet of a deuterated analog of one of the major metabolites of pentoxifylline (PTX or Trental®), is classified by FDA as a new molecular entity. PCS499 and its metabolites act on multiple pharmacological targets that are important in a variety of conditions. We have targeted Necrobiosis Lipoidica (NL) as our lead indication for PCS499. NL is a chronic, disfiguring condition affecting the skin and tissue under the skin typically on the lower extremities with no currently approved FDA treatments. NL presents more commonly in women than in men and occurs more often in people with diabetes. Ulceration occurs in approximately 30% of NL patients, which can lead to more severe complications, such as deep tissue infections and osteonecrosis threatening the life of the limb. Approximately 22,000 - 55,000 people in the United States and more than 120,000 people outside the United States are affected with ulcerated NL.

The degeneration of tissue occurring at the NL lesion site may be caused by a number of pathophysiological changes, which make it extremely difficult to develop effective treatments for this condition. Because PCS499 and its metabolites appear to affect most of the biological pathways that contribute to the pathophysiology associated with NL, PCS499 may provide a novel treatment solution for NL.

On June 18, 2018, the FDA granted orphan-drug designation for PCS499 for the treatment of NL. On September 28, 2018, the IND for PCS499 in NL became effective, such that we initiated and completed a Phase 2A multicenter, open-label prospective trial designed to determine the safety and tolerability of PCS499 in patients with NL. The study initially had a six-month treatment phase and a six-month optional extension phase. In December 2019, we informed patients and sites that the study would conclude after the treatment phase and there would no longer be an extension phase. The first enrolled NL patient in this Phase 2A clinical trial was dosed on January 29, 2019 and the study completed enrollment on August 23, 2019. The last patient visit took place in February 2020.

The primary objective of the Phase 2A trial was to evaluate the safety and tolerability of PCS499 in patients with NL and to use the safety and efficacy data to design future clinical trials. Based on toxicology studies and healthy human volunteer studies, Processa and the FDA agreed that a PCS499 dose of 1.8 grams/day would be the highest dose administered to NL patients in this Phase 2A trial. As anticipated, the PCS499 dose of 1.8 grams/day, 50% greater than the maximum tolerated dose of PTX, appeared to be well tolerated with no serious adverse events (SAEs) reported. All adverse events (AEs) reported in the study were mild in severity. As expected, gastrointestinal symptoms were the most frequent adverse events and reported in four patients, all of which resolved within 1-2 weeks of starting dosing.

Two of the twelve patients in the study presented with ulcerated NL and had ulcers for more than two months prior to dosing. At baseline, the reference ulcer in one of the two patients measured 3.5 cm2 and had completely closed by Month 2 of treatment. The second patient had a baseline reference ulcer of 1.2 cm2 which completely closed by Month 9 during the patient’s treatment extension period. In addition, while in the trial, both patients also developed small ulcers at other sites, possibly related to contact trauma, and these ulcers resolved within one month. The other ten patients, presenting with mild to moderate NL and no ulceration, had more limited improvement of the NL lesions during treatment. Historically, 13 - 20% of all the patients with NL naturally progress to complete healing over many years after presenting with NL. Although the natural healing of the ulcerated NL patients has not been evaluated independently, medical experts who treat NL patients suggest that the natural progression of an open ulcerated wound to complete closure would be significantly less than 13% over 1-2 years and probably close to 0% in patients with the larger ulcers.

| 17 |

On March 25, 2020, we met with the FDA and discussed the clinical program, as well as the nonclinical and clinical pharmacology plans to ultimately support the submission of the PCS499 New Drug Application (NDA) in the U.S. for the treatment of ulcers in NL patients. With input from the FDA, we have designed the next trial as a randomized, placebo-controlled Phase 2B study to evaluate the ability of PCS499 to completely close ulcers in patients with NL and better understand the potential response of NL patients on drug and on placebo. We have selected several clinical trial sites in the United States and are evaluating the inclusion of additional clinical trial sites, both within and outside of the United States.

On May 19, 2021, we dosed our first patient in the randomized, placebo-controlled trial and are planning an interim analysis of the data from this trial in the first half of 2022. After obtaining the results from this Phase 2B study, we expect to have an end of Phase 2 meeting with the FDA to agree on the design of the Phase 3 study, to define a Special Protocol Assessment for the Phase 3 study and to agree on the next steps to obtain approval.

PCS12852

On August 19, 2020, we in-licensed PCS12852 (formerly known as YH12852) from Yuhan Corporation (“Yuhan”), pursuant to which we acquired an exclusive license to develop, manufacture and commercialize PCS12852 globally, excluding South Korea.

PCS12852 is a novel, potent and highly selective 5-hydroxytryptamine 4 (5-HT4) receptor agonist. Other 5-HT receptor agonists with less 5-HT4 selectivity have been shown to successfully treat gastrointestinal (GI) motility disorders such as gastroparesis, chronic constipation, constipation-predominant irritable bowel syndrome, and functional dyspepsia. Less selective 5-HT4 agonists, such as cisapride, have been either removed from the market or not approved because of the cardiovascular side effects associated with the drugs binding to other receptors, especially receptors other than 5-HT4.

Two clinical studies, both which have demonstrated the effectiveness of PCS12852 on GI motility, have been previously conducted by Yuhan with PCS12852. In a Phase 1 trial (Protocol YH12852-101), the initial safety and tolerability of PCS12852 were evaluated after single and multiple oral doses in healthy subjects. PCS12852 was shown to increase GI motility in this study, increasing stool frequency with faster onset when compared to prucalopride, a less specific 5-HT4 agonist FDA-approved drug for the treatment of chronic idiopathic constipation. Based on an increase of ≥1 spontaneous bowel movement (SBM)/week from baseline during 7-day multiple dosing, the PCS12852 dose group had a higher percent of patients with an increase than the prucalopride group. All doses of PCS12852 were safe and well tolerated and no SAEs occurred during the study. The most frequently reported AEs were headache, nausea and diarrhea which were temporal, manageable, and reversible within 24 hours. There were no clinically significant changes in platelet aggregation and ECG parameters including a change in QTc prolongation in the study. In a Phase 1/2A clinical trial (Protocol YH12852-102), the safety, tolerability, gastric emptying rate and pharmacokinetics of multiple doses of a PCS12852 immediate release (IR) formulation and a delayed release (DR) formulation were evaluated. PCS12852 was safe and well tolerated after single and multiple administrations. The most frequent AEs for both the IR and DR formulations of PCS12852 were headache, nausea and diarrhea, but the incidences of these AEs were comparable with those of the 2mg prucalopride group. These AEs, which were transient and mostly mild in severity, are also commonly observed with other 5-HT4 agonists. Both formulations of PCS12852 also increased the gastric emptying rate and increased GI motility.

Yuhan had also conducted extensive toxicological studies for the product that demonstrated that the product is safe for use and can be moved into Phase 2 studies.

We plan to submit an IND application in the third quarter of 2021 based on guidance received from the FDA on the clinical development program required for patients with gastroparesis. We plan to conduct a Phase 2A randomized, placebo-controlled study in patients with gastroparesis. The purpose of the Phase 2A trial is to evaluate the safety, efficacy and pharmacokinetics of two different dosing regimens for PCS12852. Data obtained from this study will be used to better design a future Phase 2/3 efficacy study. Since patients with gastroparesis have an abnormal pattern of upper GI motility in the absence of mechanical obstruction, the Phase 2A study will be designed to evaluate the change on gastric emptying in patients with gastroparesis on the two different dosing regimens of PCS12852 compared to placebo. The only FDA-approved drug to treat gastroparesis is metoclopramide, a dopamine D2 receptor antagonist that has serious side effects and can only be used as a short-term treatment. Other 5-HT4 drugs have been used clinically but the side effects, caused mainly by binding to other receptors, has resulted in these drugs not being a viable option to treat patients with gastroparesis. It should be noted that PCS12852 is a highly specific 5-HT4 agonist that has been shown in non-clinical studies to have a cardiovascular side effect only at concentrations greater than 1,000 times the maximum concentration seen in humans.

| 18 |

PCS3117

On June 16, 2021, we executed a License Agreement with Ocuphire Pharma, Inc. (“Ocuphire Agreement”) under which provided us with an exclusive worldwide license to research, develop and commercialize PCS3117 (formerly RX-3117) globally, excluding Republic of Singapore, China, Hong Kong, Macau and Taiwan.

PCS3117 is a novel, investigational, oral small molecule nucleoside compound. PCS3117 is an analog of the endogenous nucleoside, Cytidine, and an analog of the cancer drug gemcitabine. Once intracellularly activated (phosphorylated) by the enzyme UCK2, it is incorporated into the DNA or RNA of cells and inhibits both DNA and RNA synthesis, which induces apoptotic cell death of tumor cells. PCS3117 has received orphan drug designation from the Food and Drug Administration and the European Commission for the treatment of patients with pancreatic cancer.

Gemcitabine is presently used as first line therapy for metastatic pancreatic cancer and non-small cell lung cancer, as well as used as second line therapy for other types of cancer. The difference between PCS3117 and gemcitabine is how they are activated to cancer killing nucleotides. PCS3117 also has additional pharmacological pathways which will result in cancer cell apoptosis. Since 45% - 85% of pancreatic cancer and non-small cell lung cancer patients are inherently resistant or acquire resistance to gemcitabine, the differences between PCS3117 and gemcitabine could potentially provide a therapeutic alternative to patients who do not respond to or will not respond to gemcitabine.

Resistance to gemcitabine or PCS3117 are likely caused by:

| ● | an increase in the CDA enzyme which breaks down gemcitabine and PCS3117, | |

| ● | a deficiency in transportation of gemcitabine or PCS3117 across the cell membrane, | |

| ● | down regulation of the activation enzyme (dCK for gemcitabine, UCK2 for PCS3117), | |

| ● | a change in ribonucleotide reductase activity, and | |

| ● | non-genetic influences that alter gene expression |

PCS3117 has shown broad spectrum anti-tumor activity against over 100 different human cancer cell lines and efficacy in 17 different mouse xenograft models. In preclinical trials, PCS3117 retained its anti-tumor activity in human cancer cell lines made resistant to the anti-tumor effects of gemcitabine. In August 2012, the completion of an exploratory Phase 1 clinical trial of PCS3117 in cancer patients to investigate the oral bioavailability, safety and tolerability of the compound was reported. In that study, oral administration of a 50 mg dose of PCS3117 indicated an oral bioavailability of 56% and a plasma half-life (T1/2) of 14 hours. In addition, PCS3117 appeared to be well tolerated in all subjects throughout the dose range tested.

Final results from a Phase 1B clinical trial of PCS3117 were presented in June 2016 showing evidence of single agent activity. Patients in the study had generally received four or more cancer therapies prior to enrollment. In this study, 12 patients experienced stable disease persisting for up to 276 days and three patients showed evidence of tumor burden reduction. A maximum tolerated dose of 700 mg was identified in the study. At the doses tested, PCS3117 appeared to be well tolerated with a predictable pharmacokinetic profile following oral administration.

In March 2016, a multi-center Phase 2A clinical trial of PCS3117 in patients with relapsed or refractory pancreatic cancer was initiated to further evaluate safety and efficacy. The study was designed as a two-stage study with 10 patients in stage 1 and an additional 40 patients in stage 2. According to pre-set criteria, if greater than 20% of the patients had an increase in progression free survival of more than four months, or an objective clinical response rate and reduction in tumor size, additional pancreatic cancer patients would be enrolled into stage 2. Secondary endpoints included time to disease progression, overall response rate and duration of response, as well as pharmacokinetic assessments and safety parameters. In January 2018, the final data from this trial showed evidence of tumor shrinkage in some patients with metastatic pancreatic cancer that was resistant to gemcitabine and who had failed on multiple prior treatments was presented. In this study, 31% of patients experienced progression free survival for two months or more and five patients, or 12%, had disease stabilization for greater than four months. Although the pre-set criteria of 20% of the patients having an increase in progression free survival for four months was not met, some of the gemcitabine refractory patients did respond to PCS3117. However, an evaluation of why patients were resistant to PCS3117 was not undertaken within the study.

| 19 |

In November 2017, a Phase 2A trial of PCS3117 in combination with ABRAXANE in patients newly diagnosed with metastatic pancreatic cancer was initiated. The multicenter, single-arm, open-label study is designed to evaluate PCS3117 in combination with ABRAXANE in first line metastatic pancreatic cancer patients. In February 2019, the target enrollment of 40 evaluable patients in this trial was reached. As of July 24, 2019, an overall response rate of 23% had been observed in 40 patients that had at least one scan on treatment. Preliminary and unaudited data indicated that the median progression free survival for patients in the study was approximately 5.4 months. The most commonly reported related adverse events were nausea, diarrhea, fatigue, alopecia, decreased appetite, rash, vomiting and anemia. Again, evaluation of the cause of treatment resistance to PCS3117 was not undertaken.

In order to identify patients who would more likely respond to PCS3117 than gemcitabine, we will be refining existing assays and developing new assays of biological molecules (i.e., biomarkers) over the next 6-12 months that could help to identify which patients with pancreatic cancer or non-small cell lung cancer are more likely to respond to or activate PCS3117 over gemcitabine.

PCS6422

On August 23, 2020, we in-licensed PCS6422 from Elion Oncology, Inc. (“Elion”), pursuant to which we acquired an exclusive license to develop, manufacture and commercialize PCS6422 globally.

PCS6422 is an oral, potent, selective and irreversible inhibitor of dihydropyrimidine dehydrogenase (DPD), the enzyme that rapidly metabolizes a common chemotherapy drug known as 5-FU, into inactive metabolites, such as α-fluoro-β-alanine (F-Bal). F-Bal is a metabolite that has no anti-cancer activity but causes unwanted side effects, which notably leads to dose interruptions and significantly affect a patient’s quality of life. F-Bal is thought to cause the neurotoxicity and Hand–Foot Syndrome (HFS) associated with 5-FU, and greater formation of F-Bal appears to be associated with a decrease in the antitumor activity of 5-FU. HFS can affect activities of daily living, quality of life, and requires dose interruptions/adjustments and even therapy discontinuation resulting in suboptimal tumor effects. We believe that the inhibition of DPD by PCS6422 will significantly reduce 5-FU side effects related to F-Bal. One dose of PCS6422 irreversibly blocks DPD activity for up to two weeks until DPD levels recover via de novo synthesis. Thus, we believe inhibition of DPD will result in an improved safety profile given the decrease in F-Bal and potentially higher 5-FU intra-tumoral anti-cancer metabolites that could improve efficacy.

Fluoropyrimidines (e.g., 5-FU) remain the cornerstone of treatment for many different types of cancers, either as monotherapy or in combination with other chemotherapy agents by an estimated two million patients annually. Xeloda®, the brand name of capecitabine, is an oral pro-drug of 5-FU and approved as first-line therapy for metastatic colorectal and breast cancer. However, its use is limited by adverse effects such as the development of HFS in up to 60% of patients.

Elion evaluated the potential for the combination of PCS6422 with capecitabine as a treatment of advanced gastrointestinal (GI) tumors. Nonclinical efficacy data indicated that in colorectal cancer models, pretreatment with PCS6422 enhanced the antitumor activity of capecitabine. PCS6422 dramatically increased the antitumor potency of capecitabine without increasing the toxicity. The antitumor efficacy of the combination of PCS6422 and capecitabine was tested in several xenograft animal models with human breast, pancreatic and colorectal cancer cells. These preclinical xenograft models demonstrate that PCS6422 potentiates the antitumor activity of capecitabine and significantly reduces the dose of capecitabine required to be efficacious.

Other DPD enzyme inhibitors (e.g. Gimeracil used in Teysuno® approved only outside the US) act as competitive reversible inhibitors. These agents must be present when 5-FU or capecitabine are administered to inhibit 5-FU breakdown by DPD in order to improve the efficacy and safety profiles of 5-FU. Given the reversible nature of their effect on DPD, over time 5-FU metabolism to F-Bal will return if the reversible inhibitor is not present, decreasing the amount of 5-FU in the cancer cells and decreasing the potential cytotoxicity on the cancer cells. There is also evidence that administering DPD inhibitors directly with 5-FU may also decrease the antitumor effect of the 5-FU. Because PCS6422 is an irreversible inactivator of DPD, it can be dosed the day before capecitabine administration and its effect on DPD can last longer than the reversible DPD inhibitors and beyond the time 5-FU exists in the cancer cell, even after PCS6422 has been completely eliminated out of the body. We believe this can optimize the potential cytotoxic effect and minimize the catabolism of 5-FU to F-Bal.

| 20 |

Prior to Elion’s involvement, two multicenter Phase 3 studies were conducted in patients with colorectal cancer with PCS6422 administered in 10-fold excess to 5-FU and administered with the 5-FU. Unfortunately, we believe the dose of PCS6422 during these trials was not optimal and that PCS6422 was not administered early enough to irreversibly affect the DPD enzyme, thus the regimen tended to produce less antitumor benefit than the control arm with the standard regimen of 5-FU/leucovorin (LV) without PCS6422. Later preclinical work suggested that when PCS6422 was present at the same time as and in excess to 5-FU, it diminished the antitumor activity of 5-FU, which we believe supports the proposed dosing PCS6422 several hours before 5-FU to allow PCS6422 to be cleared before the administration of 5-FU.

Elion met with the FDA in 2019 and agreed upon the clinical development program required for the combination of PCS6422 and capecitabine as first-line therapy for metastatic colorectal cancer when treatment with fluoropyrimidine therapy alone is preferred. On May 17, 2020, an IND for the Phase 1B study was granted safe to proceed by the FDA. This Phase 1B study will evaluate: i) the safety and tolerability of escalating doses of capecitabine with a fixed dose of PCS6422 in advanced GI tumor patients; ii) the pharmacokinetics of PCS6422, capecitabine, 5-FU and selected metabolites; iii) the activity of DPD over time after PCS6422 administration; and iv) the maximum tolerated dose in up to 30 patients over multiple cycles. We have selected several clinical trial sites in the United States for the study, which began patient recruitment in the first half of 2021. On August 2, 2021, we enrolled the first patient in the study.

PCS11T

On May 24, 2020, we in-licensed PCS11T (formerly known as ATT-11T) from Aposense, Ltd. (“Aposense”), pursuant to which we were granted Aposense’s patent rights and Know-How to develop and commercialize their next generation irinotecan cancer drug, PCS11T.

PCS11T is a novel lipophilic anti-cancer pro-drug that is being developed for the treatment of the same solid tumors as prescribed for irinotecan. This pro-drug is a conjugate of a specific proprietary Aposense molecule connected to SN-38, the active metabolite of irinotecan. The proprietary molecule in PCS11T has been designed to allow PCS11T to bind to cell membranes to form an inactive pro-drug depot on the cell with SN-38 preferentially accumulating in the membrane of tumors cells and the tumor core. This unique characteristic may make the therapeutic window of PCS11T wider than other irinotecan products such that the antitumor effect of PCS11T could occur at a much lower dose with a milder adverse effect profile than irinotecan. Despite the widespread use of commercially marketed irinotecan products in the treatment of metastatic colorectal cancer and other cancers resulting in peak annual sales of approximately $1.1 billion, irinotecan has a narrow therapeutic window and includes an FDA “Black Box” warning for both neutropenia and severe diarrhea. There is, therefore, a substantial unmet need to overcome the limitations of the current commercially marketed irinotecan products, improving efficacy and reducing the severity of treatment emergent AEs. We believe the potential wider therapeutic window of PCS11T will likely lead to more patients responding with less side effects when on PCS11T compared to other irinotecan products.

Pre-clinical studies conducted to date showed that PCS11T demonstrated tumor eradication at much lower doses than irinotecan across various tumor xenograft models. PCS11T does not affect acetyl choline esterase (AChE) activity in human and rat plasma in vitro, which would suggest that PCS11T will show an improved safety profile, compared to irinotecan, which is known for its cholinergic-related side effects.

We are currently planning to manufacture the product at a GMP facility, conduct the required toxicological studies required to file the IND and initiate the Phase 1B study in oncology patients with solid tumors in 2022.

Impact of COVID-19

The COVID-19 pandemic has created uncertainties in the expected timelines for clinical stage biopharmaceutical companies such as ours, including possible delays in clinical trials and disruptions in the supply chain for raw materials used in clinical trial work. Such delays could materially impact our business in future periods. Furthermore, the spread of COVID-19, which has caused a broad impact globally, may materially affect us economically. While the economic impact brought by, and the duration of, COVID-19 is difficult to assess or predict, the COVID-19 pandemic and its resulting variants could result in further disruption of global financial markets, reducing our ability to access capital, which could negatively affect our liquidity. Policymakers around the globe have responded with fiscal policy actions to support the healthcare industries and economies as a whole. Whether this support continues is uncertain. Accordingly, the extent to which the COVID-19 global pandemic impacts our business, results of operations and financial condition will depend on future developments, which are highly uncertain and are difficult to predict. These developments include, but are not limited to, the duration and spread of the outbreak, its resulting variants, its severity, the actions to contain the virus or address its impact, U.S. and foreign government actions to respond to the reduction in global economic activity, and how quickly and to what extent normal economic and operating conditions can resume. For more information on the risks associated with COVID-19, refer to Part I, Item 1A, “Risk Factors” in our Annual Report on Form 10-K.

| 21 |

Results of Operations

Comparison of the three and six months ended June 30, 2021 and 2020

The following table summarizes our net loss during the periods indicated:

| Three Months Ended | Six Months Ended | |||||||||||||||||||||||

| June 30, | June 30, | |||||||||||||||||||||||

| 2021 | 2020 | Change | 2021 | 2020 | Change | |||||||||||||||||||

| Operating Expenses | ||||||||||||||||||||||||

| Research and development expenses | $ | 1,614,954 | $ | 427,109 | $ | 1,187,845 | $ | 3,086,401 | $ | 928,855 | $ | 2,157,546 | ||||||||||||

Acquisition of in-process research and development |

515,630 | - | 515,630 | 515,630 | - | 515,630 | ||||||||||||||||||

| General and administrative expenses | 1,329,213 | 374,878 | 954,335 | 2,051,073 | 859,255 | 1,191,818 | ||||||||||||||||||

| Operating Loss | (3,459,797 | ) | (801,987 | ) | (5,653,104 | ) | (1,788,110 | ) | ||||||||||||||||

| Other Income (Expense) | ||||||||||||||||||||||||

| Forgiveness of PPP loan and related accrued interest | 163,771 | - | 163,771 | 163,771 | - | 163,771 | ||||||||||||||||||

| Interest expense | - | (19,280 | ) | 19,280 | (362 | ) | (36,450 | ) | 36,088 | |||||||||||||||

| Interest income | 1,814 | 18 | 1,796 | 6,755 | 846 | 5,909 | ||||||||||||||||||

| Net Operating Loss Before Income Tax Benefit | (3,294,212 | ) | (821,249 | ) | (5,482,940 | ) | (1,823,714 | ) | ||||||||||||||||

| Income Tax Benefit | 137,169 | 87,835 | 49,334 | 226,417 | 215,964 | 10,453 | ||||||||||||||||||

| Net Loss | $ | (3,157,043 | ) | $ | (733,414 | ) | $ | (5,256,523 | ) | $ | (1,607,750 | ) | ||||||||||||

Revenues.

We do not currently have any revenue under contract or any immediate sales prospects.

Research and Development Expenses.

Our research and development costs are expensed as incurred. Research and development expenses include (i) licensing of compounds for product testing and development, (ii) program and testing related expenses, (iii) amortization of the exclusive license intangible asset used in research and development activities, and (iv) internal research and development staff related payroll, taxes and employee benefits, external consulting and professional fees related to the product testing and our development activities. Non-refundable advance payments for goods and services to be used in future research and development activities are recorded as prepaid expenses and expensed when the research and development activities are performed.

| 22 |

During the three months ended June 30, 2021 and 2020, we incurred total research and development expenses of $1,614,954 and $427,109, respectively. Research and development expenses were $3,086,401 and $928,855 for the six months ended June 30, 2021 and 2020, respectively. Costs for the three and six months ended June 30, 2021 and 2020 were as follows:

Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2021 | 2020 | 2021 | 2020 | |||||||||||||

| Amortization of intangible assets | $ | 198,832 | $ | 198,832 | $ | 397,664 | $ | 397,664 | ||||||||

| Research and development salaries and benefits | 453,721 | 114,579 | 702,390 | 254,851 | ||||||||||||

| Preclinical, clinical trial and other costs | 962,401 | 113,698 | 1,986,347 | 276,340 | ||||||||||||

| Total | $ | 1,614,954 | $ | 427,109 | $ | 3,086,401 | $ | 928,855 | ||||||||

Overall, during the three months ended June 30, 2021, our research and development expenses increased by $1,187,845 when compared to the same period in 2020. The increase was primarily due to an increase in preclinical, clinical trial and other costs of $848,703, which was attributable to expenses we incurred as we commenced our Phase 2B clinical trial for PCS499, Phase 1B clinical trial for PCS6422 and for pre-IND costs for PCS12852. Expenses include costs we paid contract research organizations, for regulatory filing and maintenance fees, drug product testing and stability, consulting, and other clinical fees. During the same period in 2020, we were completing the patient portion of our Phase 2A clinical trial for PCS499 and incurring regulatory filing and consulting fees as we prepared for our meeting with the FDA. Additionally, during the six months ended June 30, 2021, we experienced increases in payroll and related costs of $339,142 from raised employee salary rates, hiring additional personnel and stock-based compensation, when compared to the same period in 2020.

During the six months ended June 30, 2021, our research and development costs increased by $2,157,546 when compared to the same period in 2020. The increase was primarily due to a $1,710,007 increase in expenses related to the clinical and pre-clinical trial costs mentioned above. Payroll and related costs increased by $447,539 during the six months ended June 30, 2021 when compared to the same period in 2020.

We anticipate our research and development costs to increase significantly in the future as we: (i) start clinical trials for PCS499 and PCS6422, as well as PCS12852 after it has been declared safe to proceed by FDA (expected later this year), including the cost of having drug product manufactured; (ii) complete a biomarker assay for PCS3117; and (iii) obtain IND enabling data for PCS11T.

The funding necessary to bring a drug candidate to market is subject to numerous uncertainties. Once a drug candidate is identified, the further development of that drug candidate may be halted or abandoned at any time due to a number of factors. These factors include, but are not limited to, funding constraints, safety or a change in market demand. For each of our drug candidate programs, we periodically assess the scientific progress and merits of the programs to determine if continued research and development is economically viable. Some programs may be terminated due to the lack of scientific progress and lack of prospects for ultimate commercialization. As noted above, we anticipate our research and development costs to increase in the future as we conduct the Phase 2B trial to evaluate the ability of PCS499 to completely close ulcers in patients with NL and begin a Phase 1B clinical trial for PCS6422. On May 19, 2019, we dosed the first patient in our PCS499 randomized, placebo-controlled trial and on August 2, 2021, we dosed the first patient in our PCS6422 trial.

Our clinical trial cost accruals are based on estimates of patient enrollment and related costs at clinical investigator sites, as well as estimates for the services received and efforts expended pursuant to contracts with multiple research institutions and CROs that conduct and manage clinical trials on our behalf.